Lehman redux: Why Trump could light the fuse as global debt time bomb ticks away

There is an ominous sense of déjà vu about the world right now which is reminiscent of a global economy out of control and heading into a new disaster. Global growth is running out of steam, world debt exposure has reached crisis proportions, while over-leveraged financial markets are looking extremely overstretched. A single major credit event like 2008’s Lehman’s collapse would be enough to tip the world back into deep catastrophe.

Next time, there might be no easy way back. Policymakers are running out of options on how to deal with any new crisis. Global interest rates are already down at rock bottom levels, the world is awash with synthetic money created by the central banks’ super-stimulus and government debt exposure is bursting at the seams. Short of prayers to St Jude, the patron saint of Lost Causes, the world’s policy cupboard is looking too bare to cope.

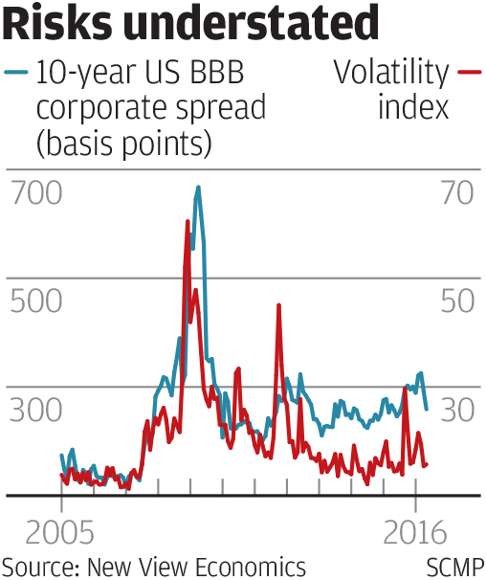

If policymakers seem to be sleepwalking into another crisis, so too are the global financial markets. Lifted by US$15 trillion of central bank pump-priming over the last seven years, global equity markets seem far removed from any deep-rooted bear market tendencies. Bond yields are close to record lows, corporate credit spreads remain relatively tight, while market fear gauges like the Vix volatility index are hardly fretting. It is fair to say that global financial markets have ‘irrational exuberance’ written all over them right now.

Some global policymakers may be ranting and railing against the potential ‘doom-loop’ that the world economy is getting itself tangled up in, but little is being done to stop the rot. Supranational bodies like the International Monetary Fund, the Bank for International Settlements and the World Bank have all warned about the explosion of global debt, but talking is one thing and direct action is something else.

Their main worry is the global recovery has become too dependent on an explosive build-up of debt thanks to all the cheap money generation in the wake of the financial crash.

Since 2007, world debt is estimated to have risen by US$57 billion, an accumulation which could have devastating future effects if it starts to sour. Households, businesses and governments have all increased debt at a time when borrowing costs have hit an all-time low. It is less of a problem as cheap money is helping the real economy by boosting consumption, investment and growth. But the chief worry is that cheap money has mainly been ramping up financial speculation in property, stocks and high-risk assets.

Once the world interest rate cycle starts to turn, this will have seismic consequences for global growth and for markets. Tighter lending conditions will drag growth as consumer spending and business output, investment and hiring plans start to stall. Higher borrowing costs will also tighten the screws for over-leveraged investors raising the risk of more than a knee-jerk correction in markets at some stage.

Confidence is key right now. In recent years, corporate debt has reached extreme levels and far exceeds pre-Lehman levels, with companies continuing to borrow like there is no tomorrow. If market confidence collapses and equity and credit markets start to crumble, the cost of capital to businesses could rise very sharply. The increased spectre of major corporate failures or debt defaults could quickly lead to very sharp hikes in credit spreads.

This would be serious news for emerging market economies (EMEs), which have been a major crucible for world economic recovery in the wake of the global crash. During the recovery process over the last six years, EMEs have become seriously overburdened by crippling debt levels and any new crisis of confidence could easily trigger investor capital outflows and spark a new financial storm. World growth prospects could suffer badly.

The global economy is sitting on a ticking time bomb which quickly needs defusing to avert another full-blown crisis. A further troubling development is that the next potential leader of the world’s biggest economy is far from being a safe pair of hands. If Republican candidate Donald Trump is elected to be the next US President in November, the world could be in deep trouble.

Trump’s maverick ideas to rid the US of its US$19 trillion Federal debt pile by ‘discounting’ could be the beginning of the end for global financial stability. It could trigger a savage reaction in global markets and the mother of all credit events.

It may be time for global investors to batten down the hatches against the approaching financial storm.

David Brown is the chief executive of New View Economics