Executive Summary

The Southeast U.S. and Texas are experiencing an economic boom, mostly due to manufacturing and energy industry growth. But that boom is at risk from unchecked climate change, which could render this region—already one of the hottest and most weather vulnerable of the country—at significant economic risk. However, if policymakers and business leaders act aggressively to adapt to the changing climate and to mitigate future impacts by reducing their carbon emissions, this region can lead in responding to climate risk. The Southeast can demonstrate to national and global political leaders the kind of strong response necessary to ensure a strong economic future.

This region, comprising the 11 Southeastern states of Alabama, Arkansas, Florida, Georgia, Kentucky, Louisiana, Mississippi, North Carolina, South Carolina, Tennessee and Virginia as well as Texas to the west, has witnessed a major recent manufacturing boom, and is poised for further economic growth in the coming years.1 In 2013, manufacturing contributed $2.1 trillion to the U.S. economy—more than 12% of GDP—and accounted for 88% of all U.S. exports, a remarkable 51% increase from declines during the last recession. The region’s economic vitality makes it one of the most productive parts of the country.

But climate change is putting that productivity at risk. While the Southeast and Texas are generally accustomed to heat and humidity, the scale of increased heat—along with other impacts such as sea level rise and storm surge—will likely cause significant and widespread economic harm, especially to a region so heavily invested in physical manufacturing, agriculture and energy infrastructure.

If we continue on our current greenhouse gas emissions pathway,2 the Southeastern U.S. and Texas will likely experience significant drops in agricultural yield and labor productivity, along with increased sea level rise, higher energy demand, and rising mortality rates. In particular, the region’s agricultural sector will be negatively influenced by the changing climatic conditions, with several commodity crops likely to face severe yield declines. Meanwhile, residents and businesses will likely be affected by higher heat-related mortality, increased electricity demand and energy costs, and declines in labor productivity, threatening the manufacturing base that is increasingly driving the regional economy. And in some cities, such as Miami and New Orleans, sea level rise will put significant amounts of existing coastal property at risk.

The mission of the Risky Business Project is to quantify the economic risks to the U.S. from unmitigated climate change. Our inaugural report, Risky Business: The Economic Risks of Climate Change in the United States,3 highlighted these impacts across every region of the country, with a focus on three sectors: agriculture, energy demand and coastal infrastructure. We also looked at overarching issues such as changes in labor productivity and heat-related mortality. This follow-up report focuses on the Southeast and Texas and offers a first step toward defining the range of potential economic consequences to this specific region if we continue on our current greenhouse gas emissions pathway.

Our research combines state-of-the-art climate science projections through the year 2100 (and beyond in some cases) with empirically derived estimates of the impact of projected changes in temperature and precipitation on the Southeastern and Texan economies. We analyze not only those outcomes most likely to occur, but also lower-probability, higher-cost climate futures. These are tail risks, most often expressed in this report as the 1-in-20 chance events. As in our other reports, we look at climate impacts at a geographically granular level.

Our findings show that if we stay on our current emissions path, the Southeast and Texas will likely experience significant economic impacts due to climate change.

- By the end of the century, the Southeast and Texas will likely experience dangerous levels of extreme heat.

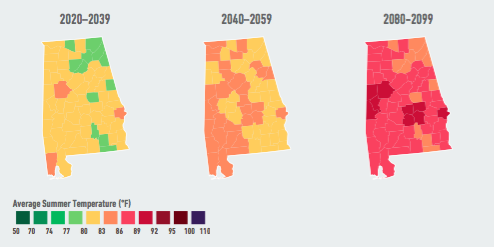

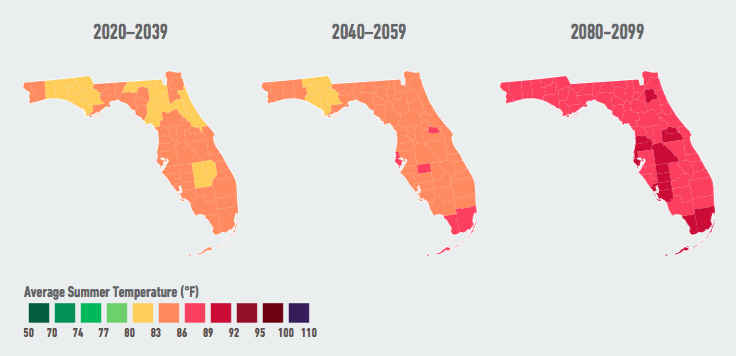

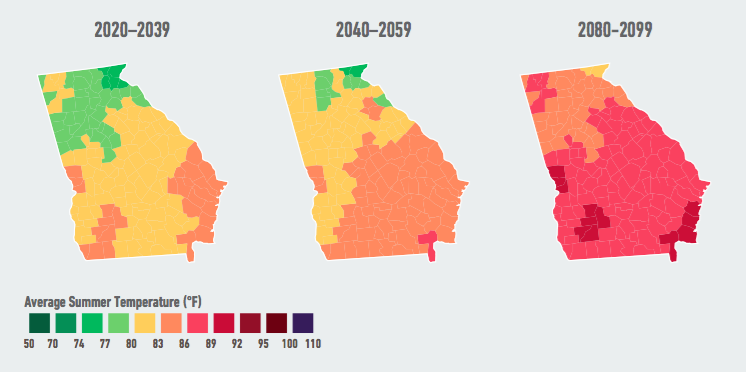

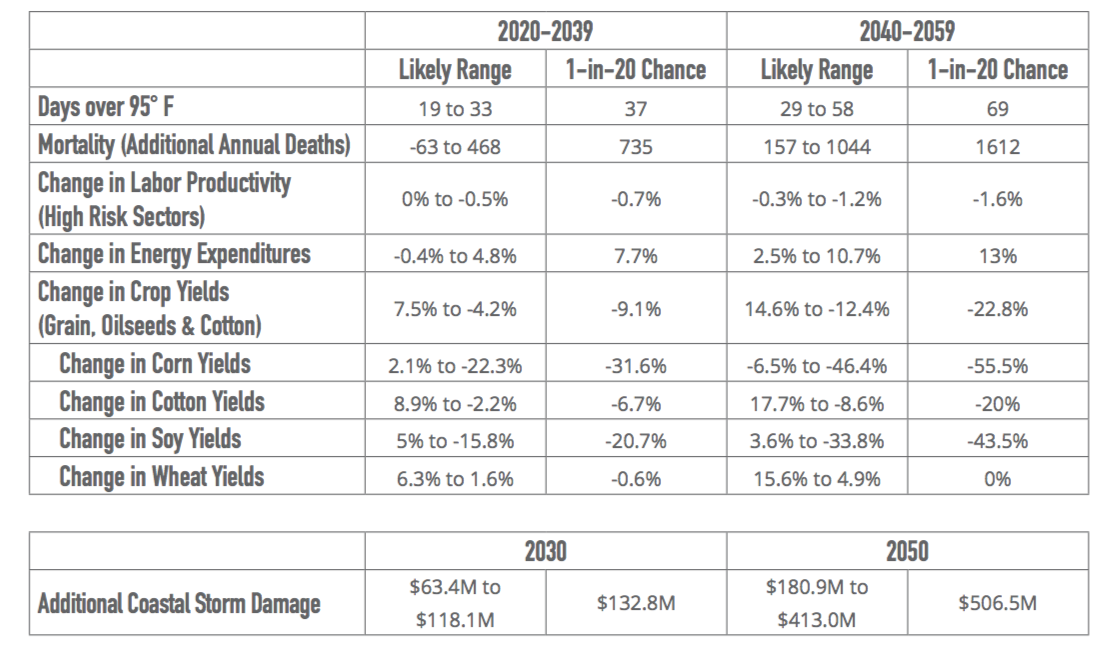

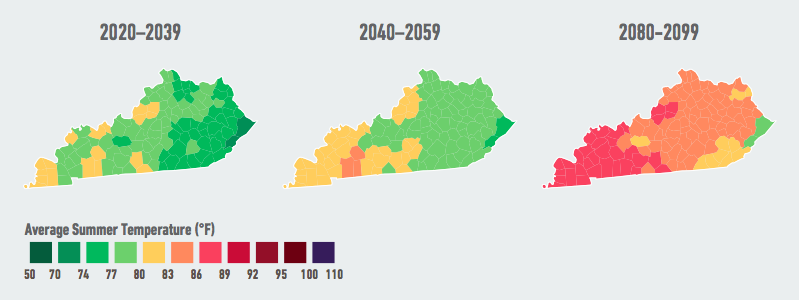

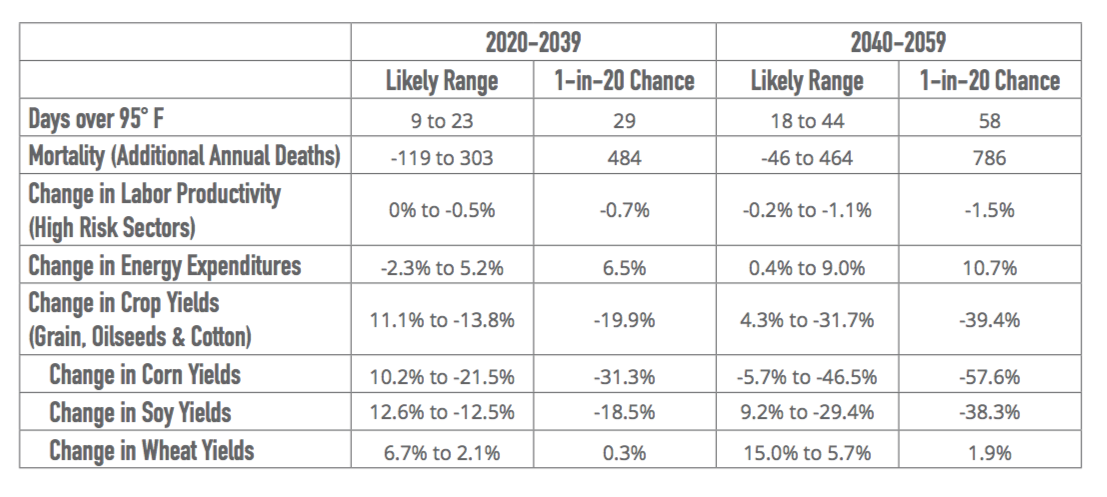

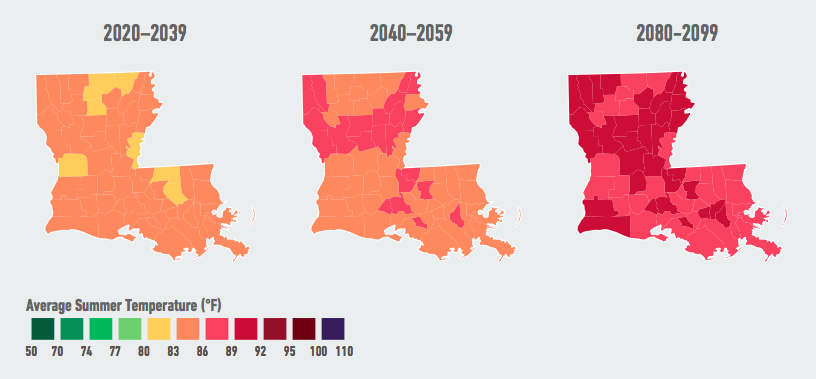

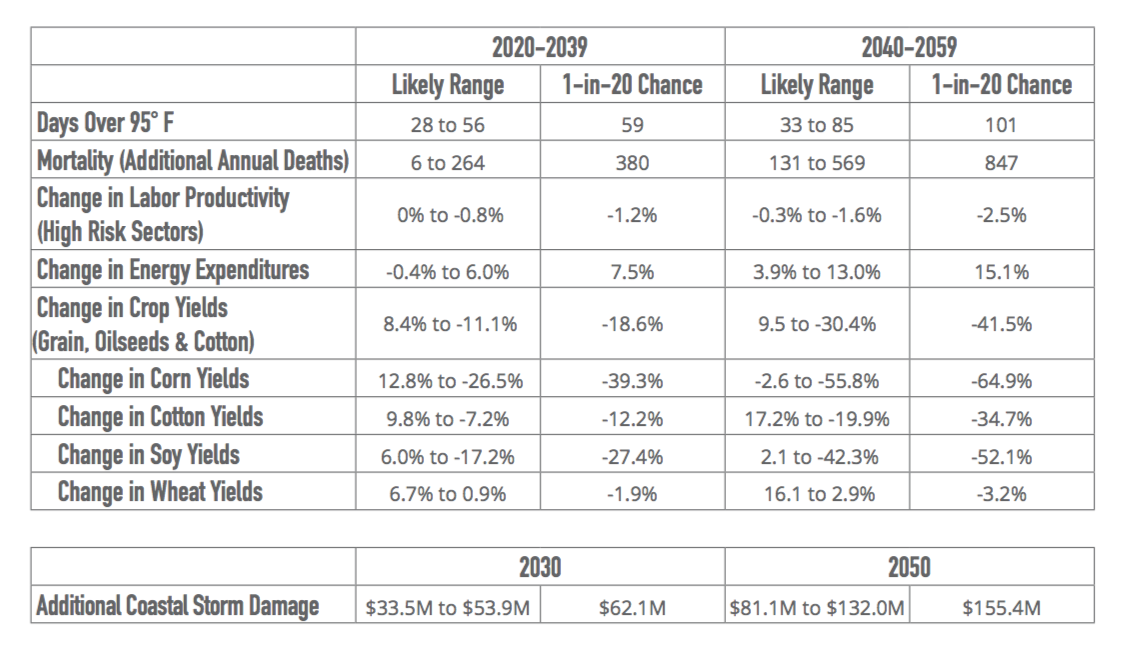

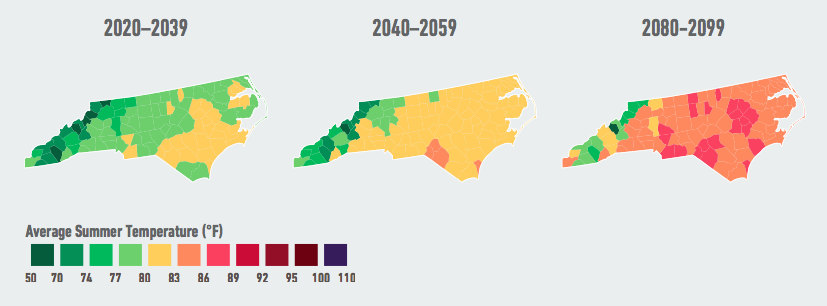

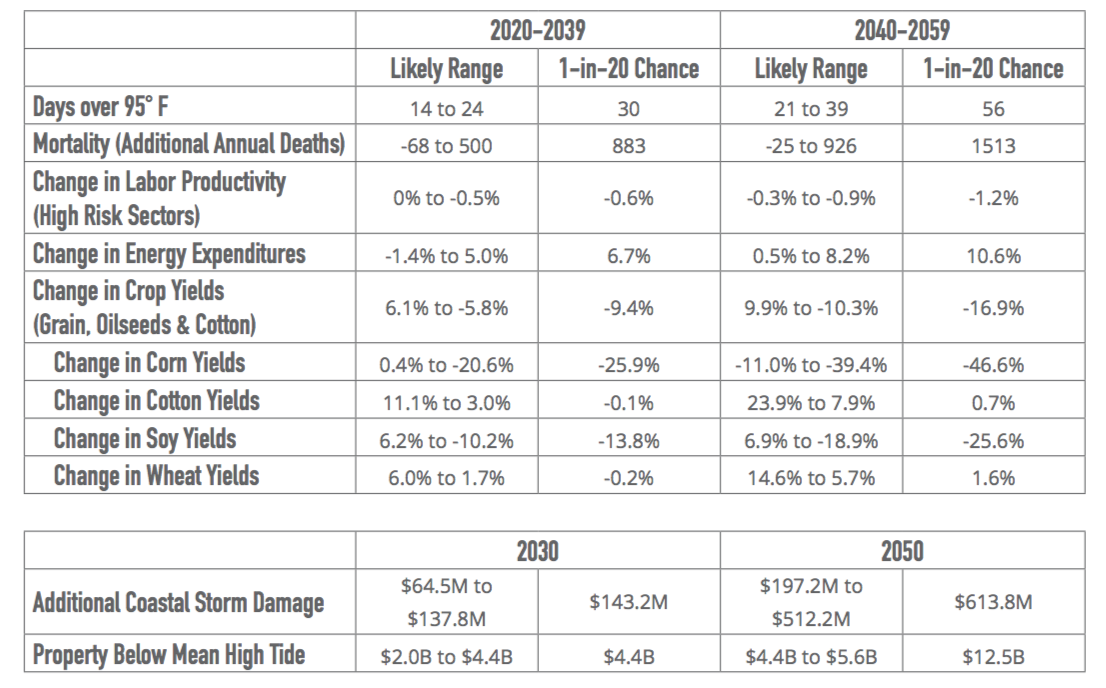

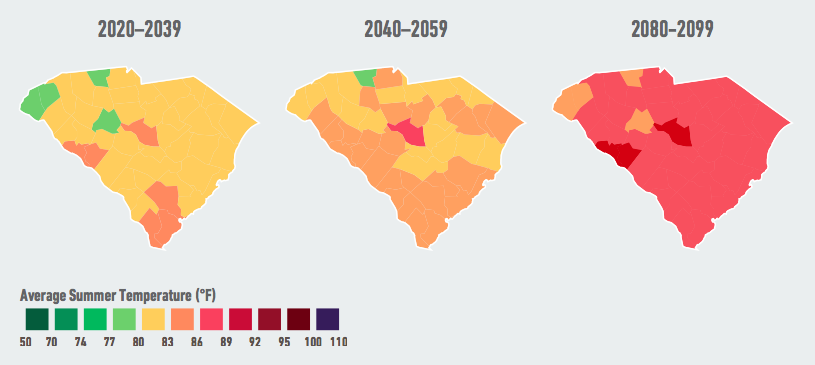

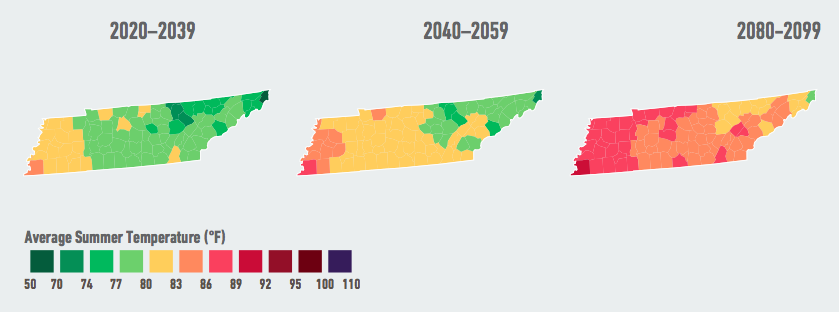

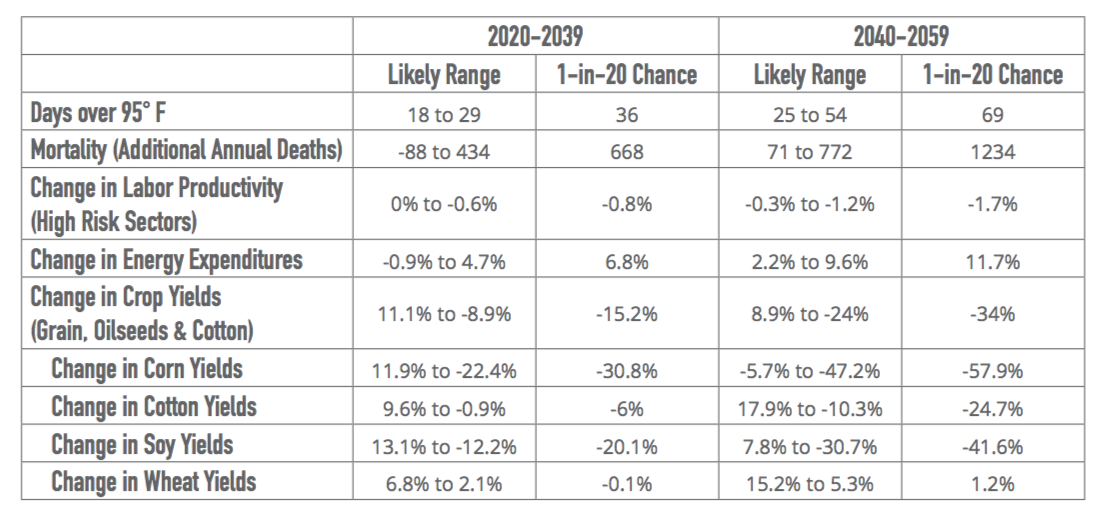

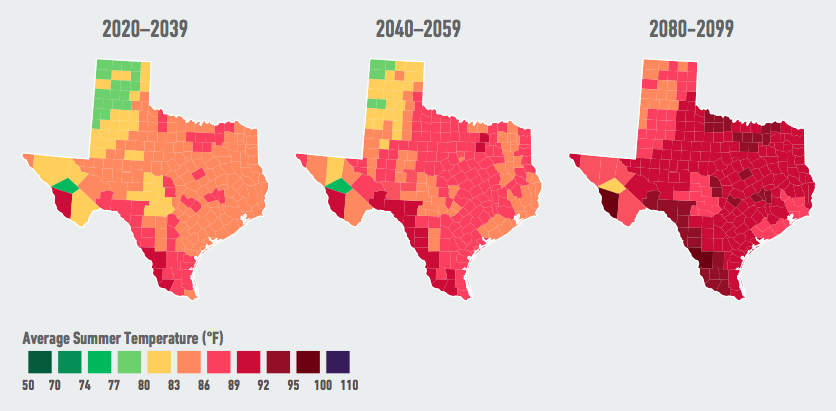

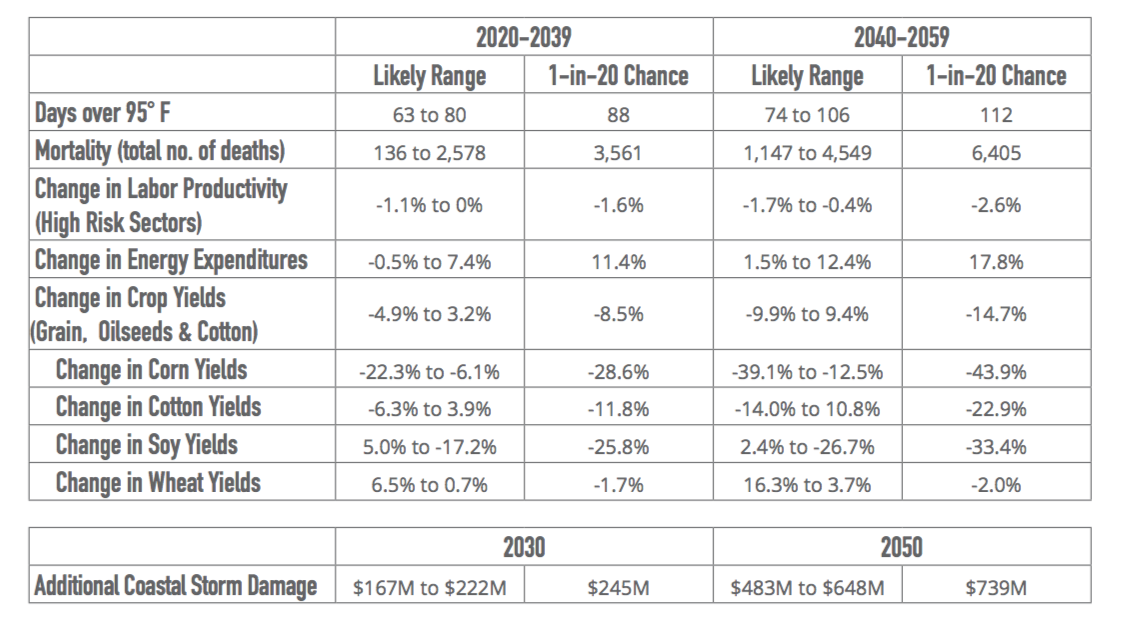

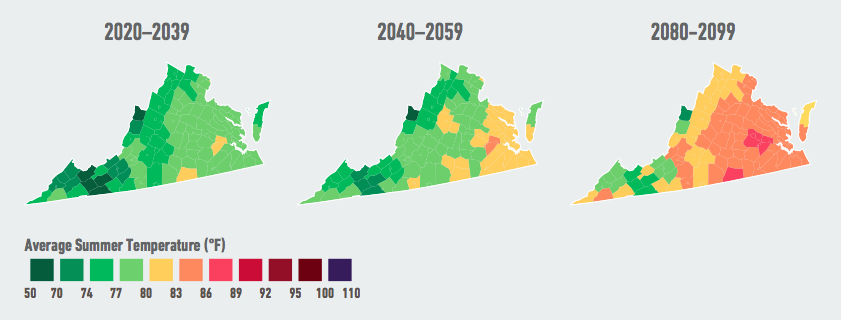

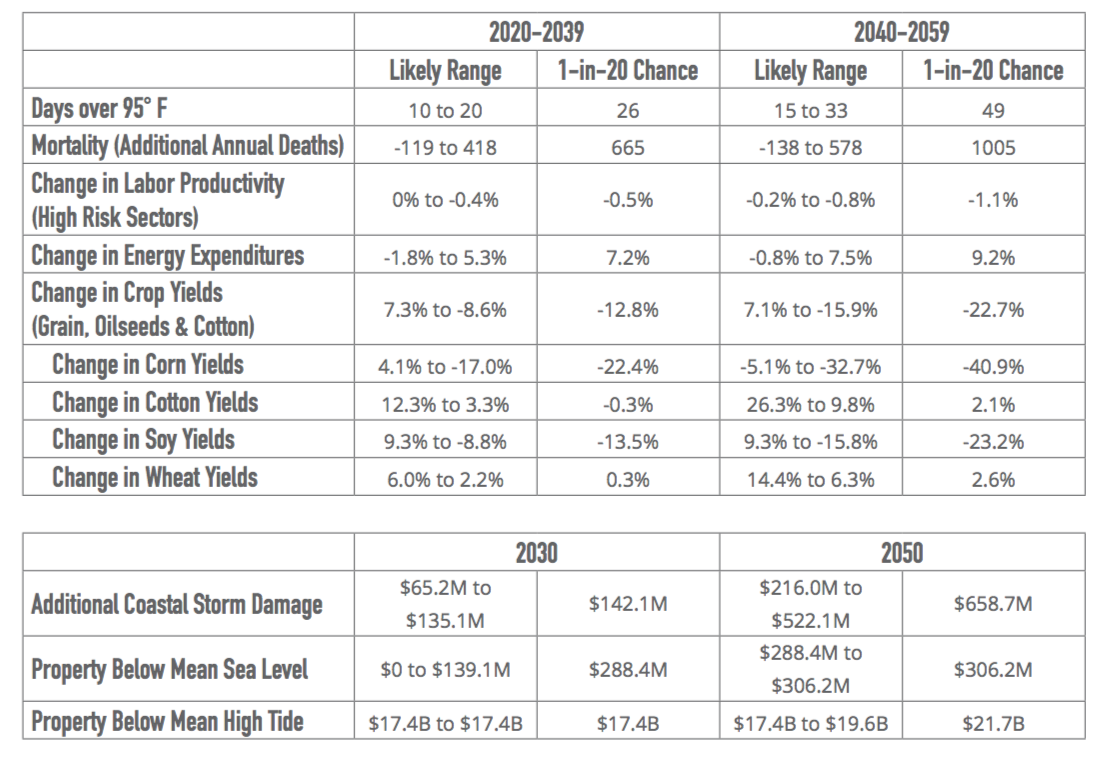

- By the end of this century, the average number of extremely hot days across the region each year—with temperatures above 95°F—will likely increase by as much as 14 times from nine days per year in recent decades to as many as 123 days per year.

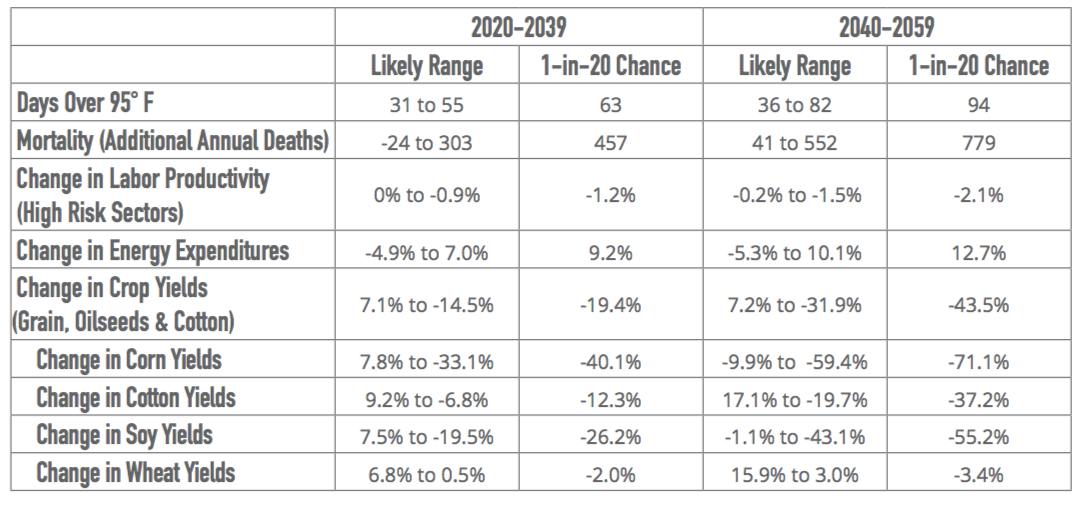

- Rising humidity combined with increased heat across the region will likely mean more frequent days that reach extremely dangerous levels on the Human Heat Stroke Index.4 By the end of the century, Florida will likely experience as many as 24 days per year with heat and humidity conditions similar to the Chicago heat wave of 1995, which caused more than 700 heat-related deaths.

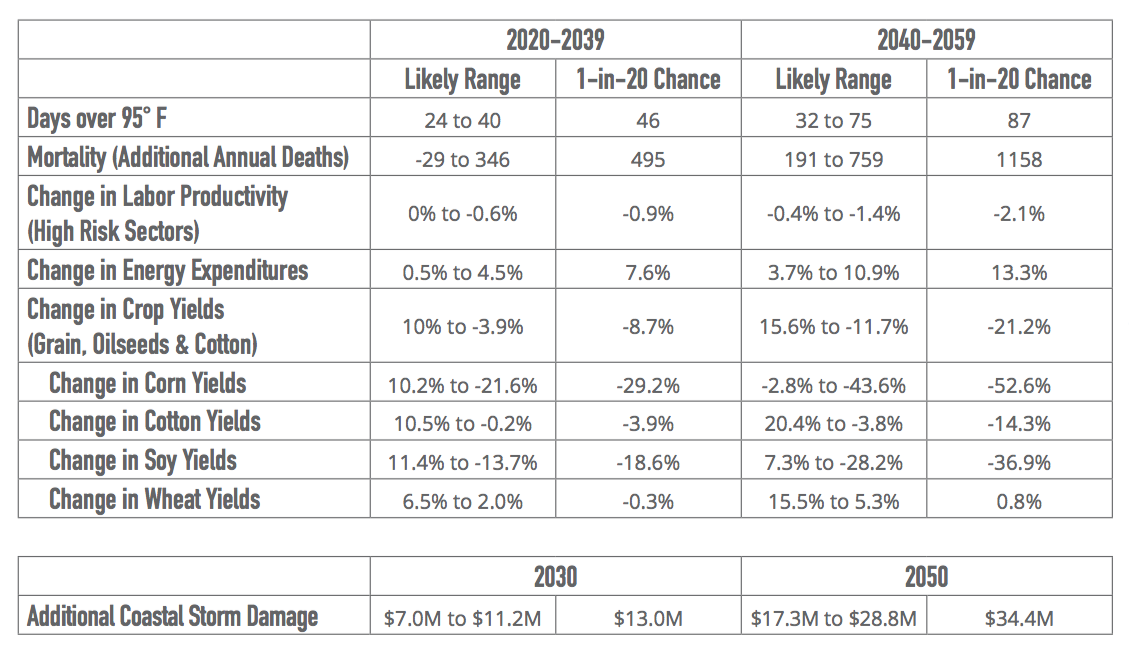

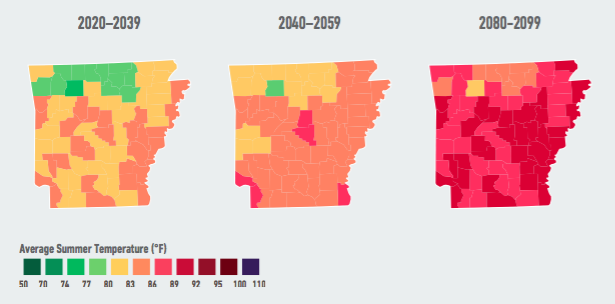

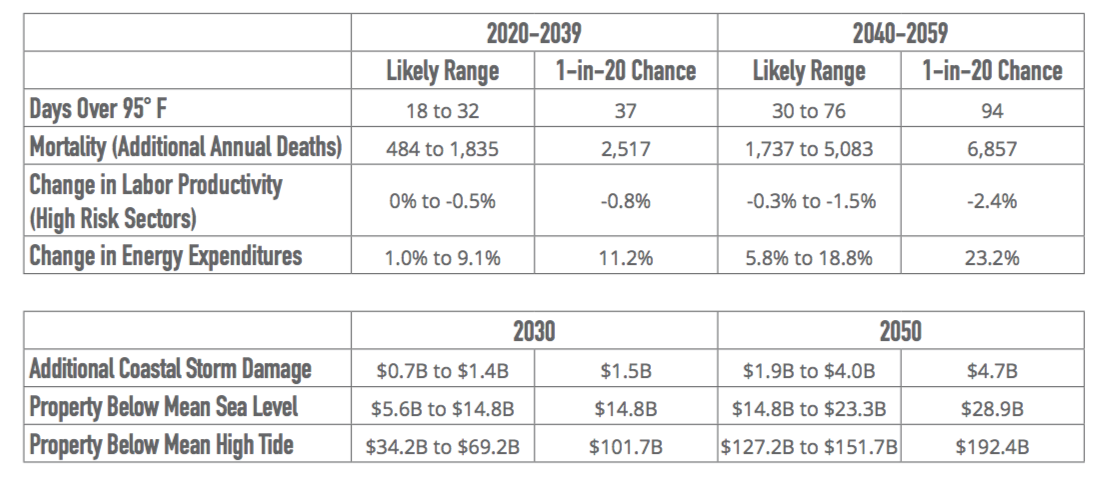

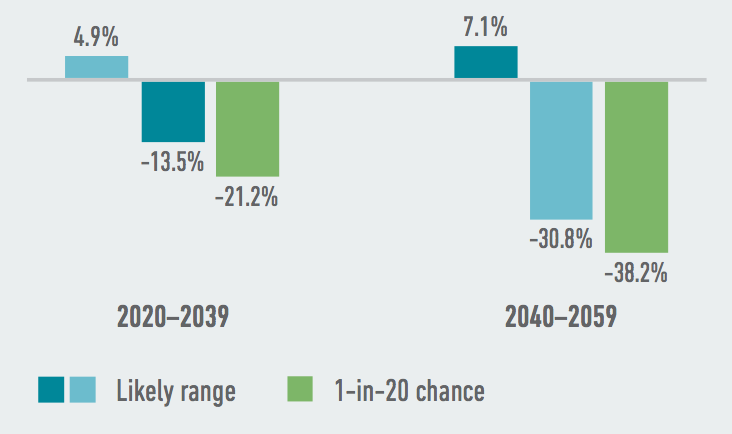

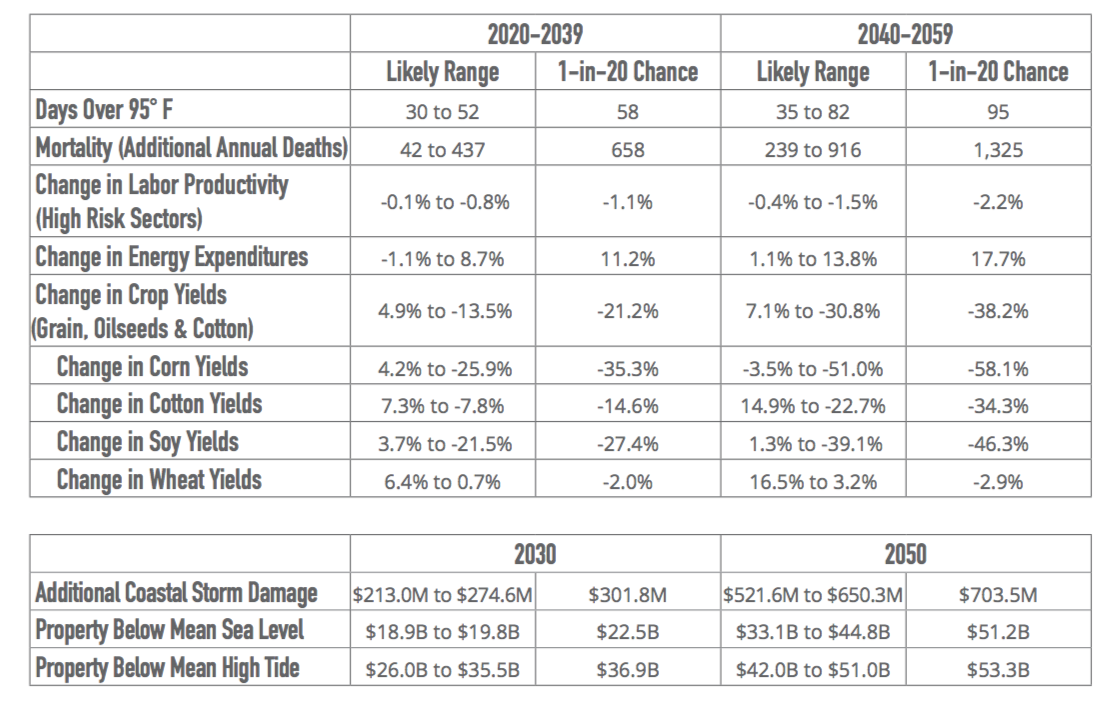

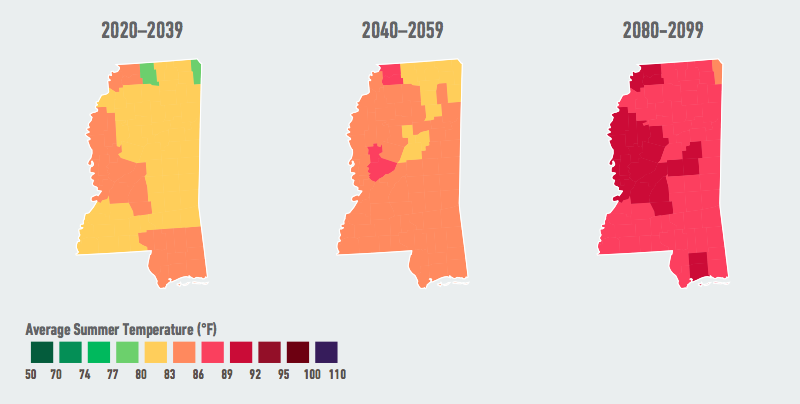

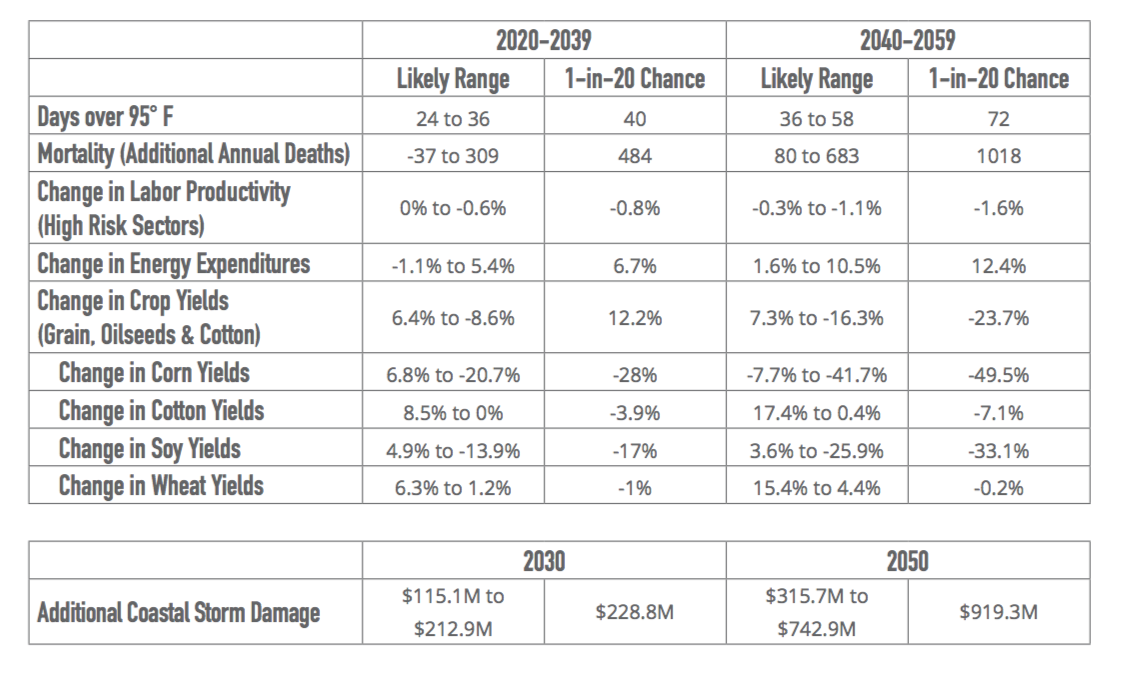

- By mid-century, the average Mississippi resident will likely experience 33 to 85 days above 95°F per year, with a 1-in-20 chance of encountering more than 101 extremely hot days—more than three full months— per year. By the end of the century, the average Arkansas resident will likely experience between 65 and 135 days above 95°F in a typical year—more extremely hot days than the average Arizonan has experienced annually in recent decades.

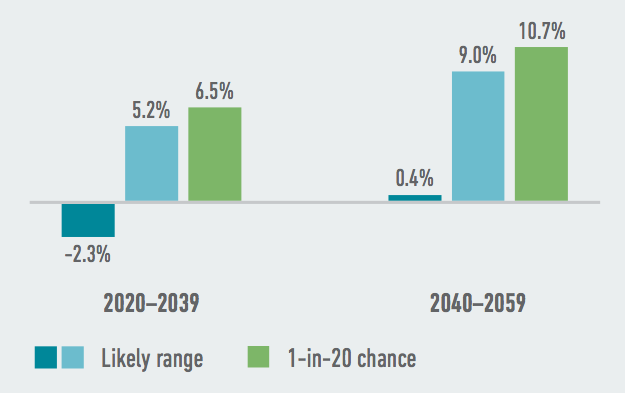

- Rising temperatures will likely lead to a surge in electricity demand, as well as to a decline in energy system efficiency in many of the manufacturing-intensive states in the Southeast and Texas.

- The Southeast and Texas are high-emitting and high energy-use regions, mainly due to their economic reliance on energy- and emission-intensive sectors such as manufacturing, agriculture, oil and gas production and mining.

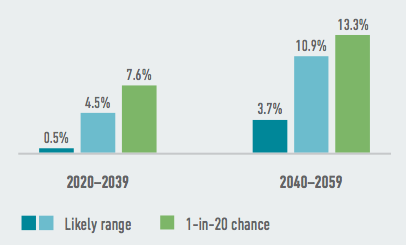

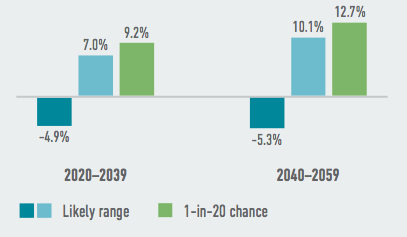

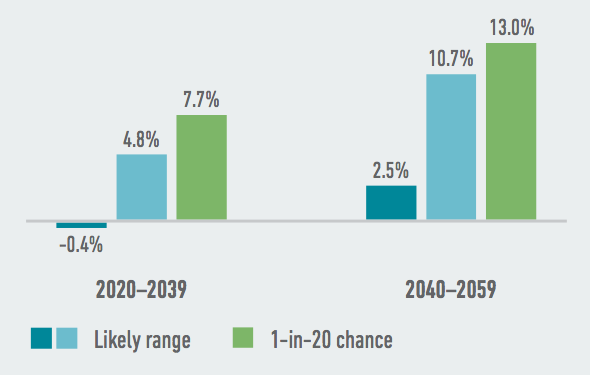

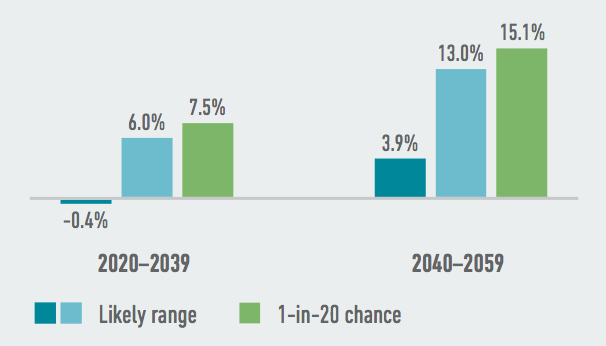

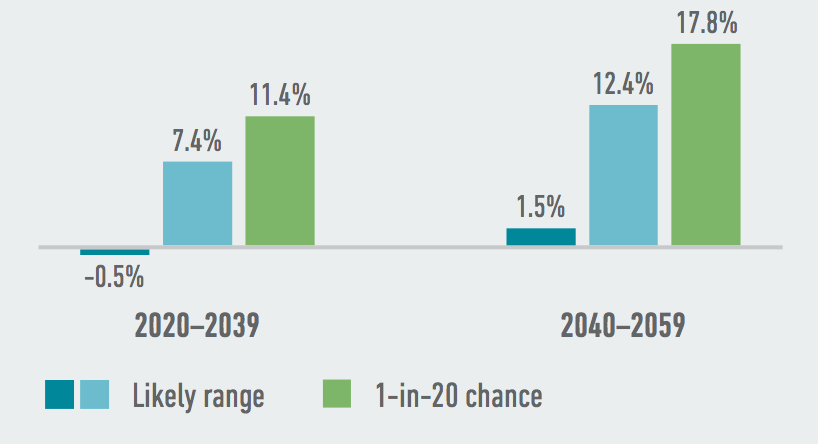

- As temperatures rise and individual households and businesses increase their use of air conditioning, electricity demand across the region will rise—with a corresponding increase in prices. The Southeast region will likely see an average increase of 4% to 12% in energy costs by mid-century, with a 1-in-20 chance these costs will increase by more than 38% by the end of the century.

- Sea level rise along the Atlantic and Gulf coasts will likely lead to large-scale losses from damage to coastal property and infrastructure.

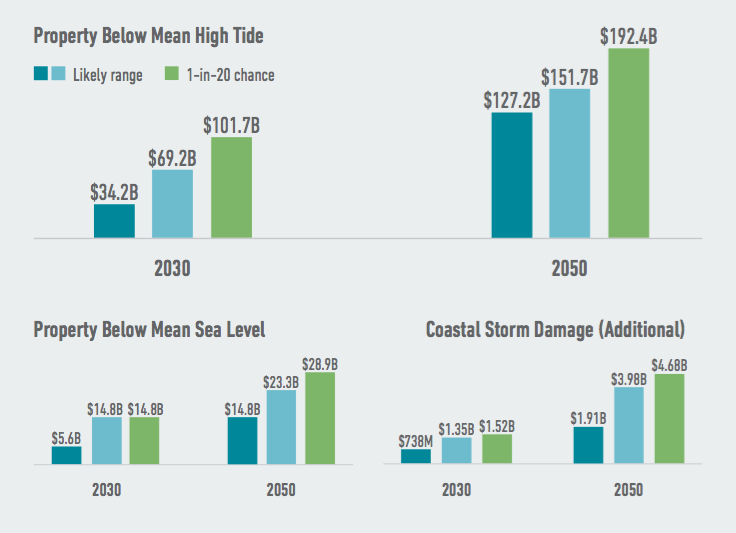

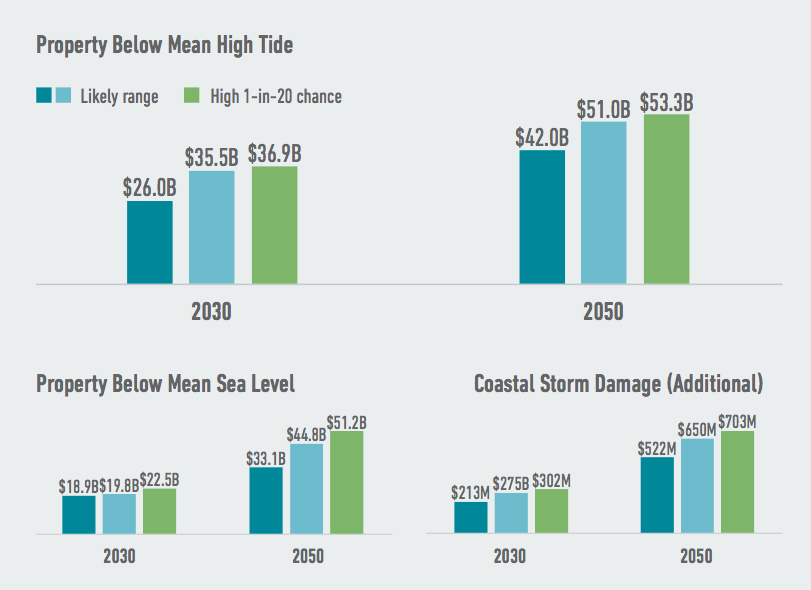

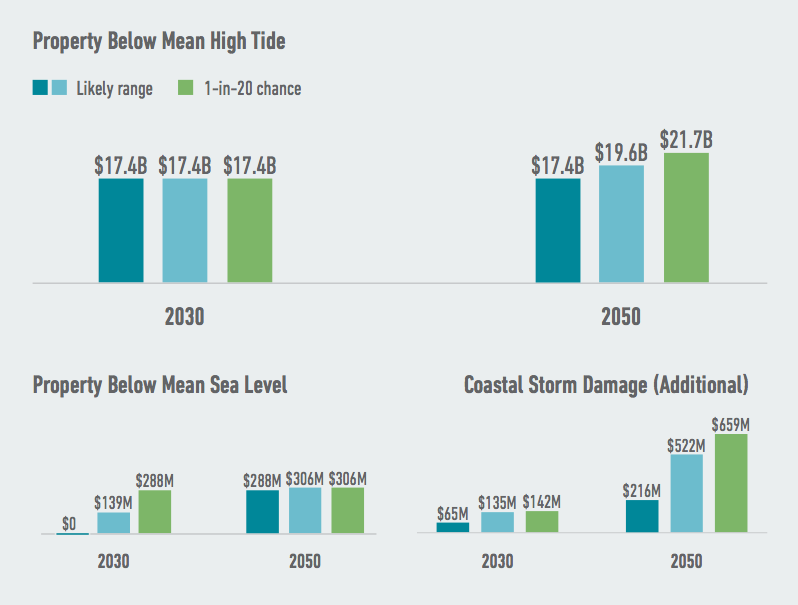

- The Southeast region faces the highest risks of coastal property losses in the nation. If we continue on our current emissions path, between $48.2 billion and $68.7 billion in existing coastal property in the Southeast will likely be below sea level by 2050, with a 1-in-100 chance of more than $107 billion in existing property at risk. Rising sea levels will also damage critical infrastructure, including water supply, energy, and transportation systems.

- Louisiana and Florida will be hit hardest by property damages due to sea level rise. By 2030, $19.8 billion in existing coastal property in Louisiana will likely be below mean sea level. By 2050, that number increases to between $33.1 billion and $44.8 billion. In Florida, losses of existing property will likely range between $5.6 billion and $14.8 billion by 2030 to between $14.8 billion and $23.3 billion by 2050.

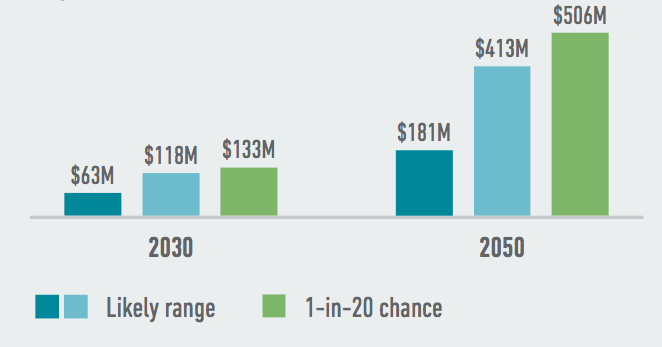

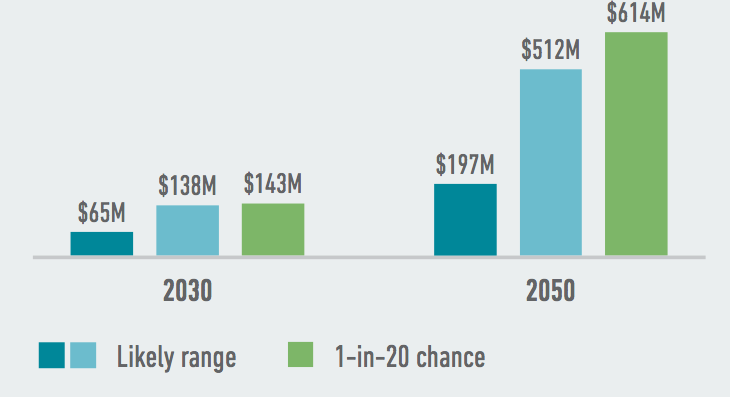

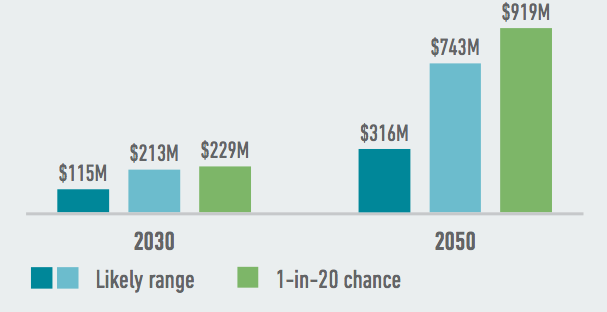

- Hurricanes and other coastal storms will interact with rising sea levels, resulting in a likely growth in average annual storm losses due to higher storm surge. By 2050, average annual losses in the Southeast will likely increase by $3.6 to $6.8 billion. Potential changes in hurricane activity could lead to even greater losses.

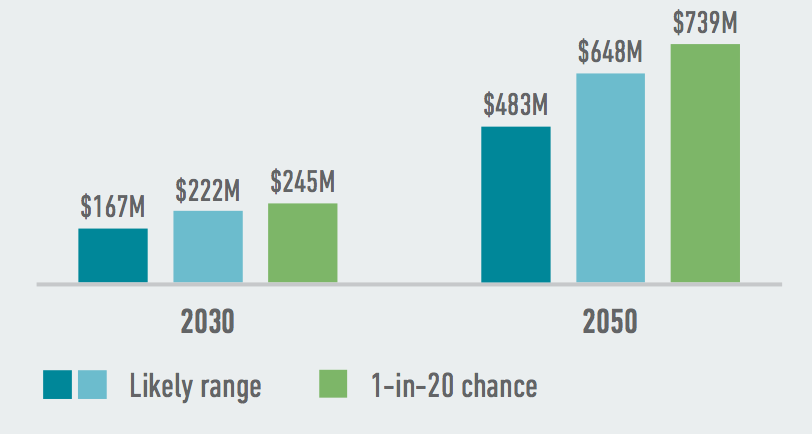

- By 2030, average annual losses from hurricanes and other coastal storms will likely increase by $167 million to $222 million in Texas. By 2050, storm losses will likely increase by $483 million to $648 million.

- Local sea level rise will vary along the coasts. At Grand Isle, Louisiana, mean sea level will likely rise 1.9 to 2.4 feet by 2050 and by 4.1 to 5.8 feet by 2100. Meanwhile, mean sea level at Charleston, South Carolina will likely rise by 0.9 to 1.4 feet by 2050 and by 2.1 to 3.8 feet by the end of the century.

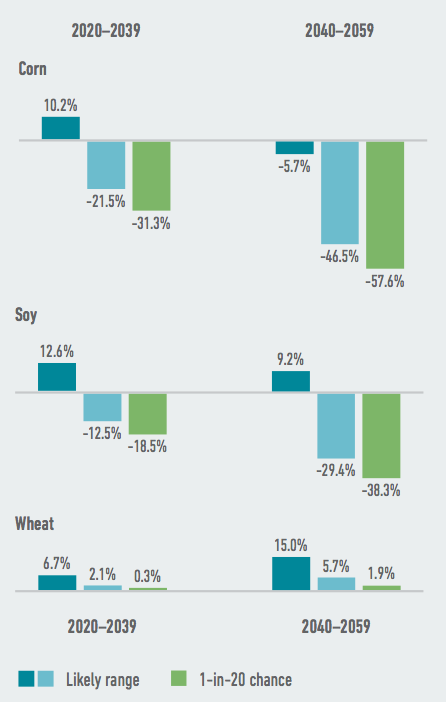

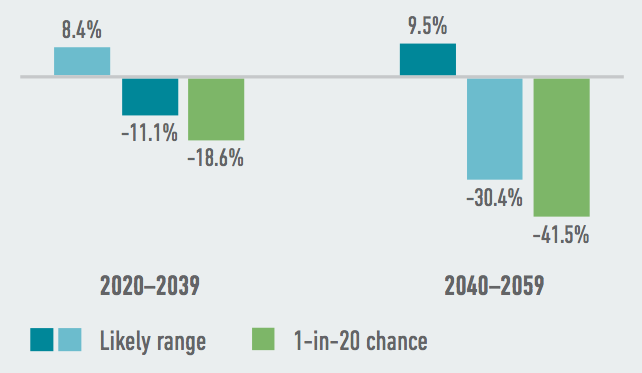

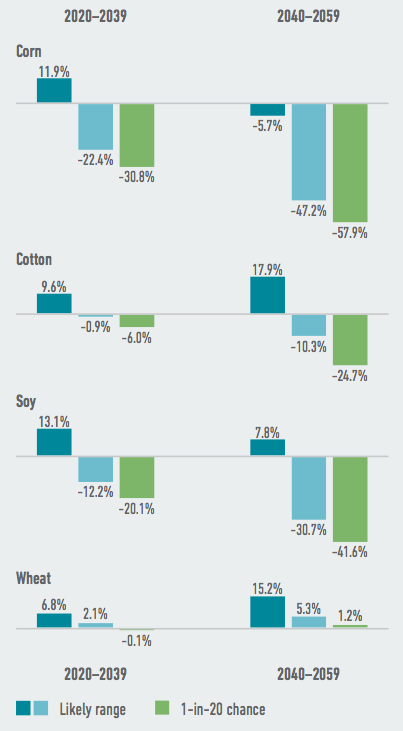

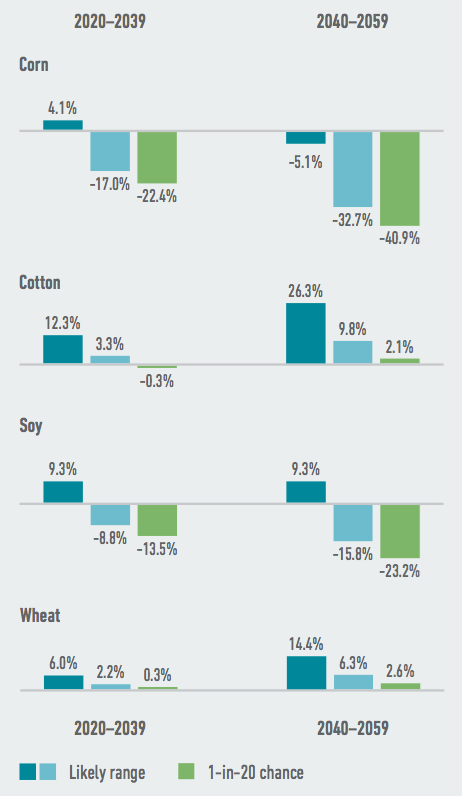

- Changes in temperature and precipitation will likely lead to changes in crop yields, with several major commodity crops facing steep potential declines.

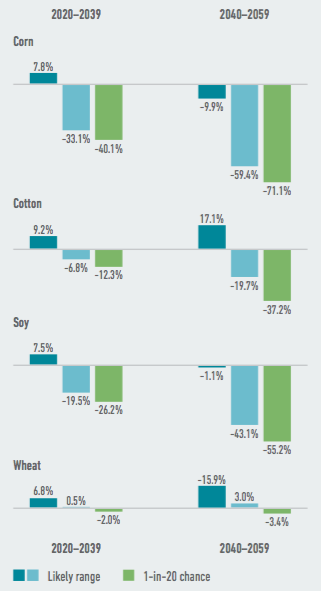

- Over the next five to 25 years, without significant adaptation by farmers, the Southeast will likely see losses in corn yields of as much as 21% and in soybean yields of as much as 14% on average across the region as a whole. By the end of the century, these crops will take an even bigger hit: Corn yields will likely decrease by as much as 86%, with a 1-in-20 chance of more than 93% decline, and soybean yields will likely decrease by as much as 76%.

- Kentucky will likely experience the third largest crop losses in the country. By mid-century, Kentucky will likely see average losses in its grain and oilseed crops of as much as 32% annually, absent adaptation. By the end of the century, Kentucky’s losses will likely increase to as much as 69% annually.

- Over the next five to 25 years, Texas will likely see corn yield declines of as much as 22% annually, absent adaptation. These losses grow to as much as 39% annually by mid-century.

- On the other hand, warmer temperatures may actually improve the growing conditions for some crops in several southeastern states. Wheat yields, for example, are likely to increase as a result of benefits from higher carbon dioxide in the atmosphere. Cotton yields will see mixed effects, with the likely range of impacts spanning yield gains to losses for many Southeastern states.

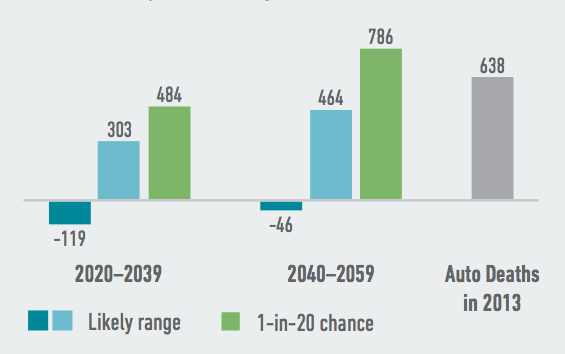

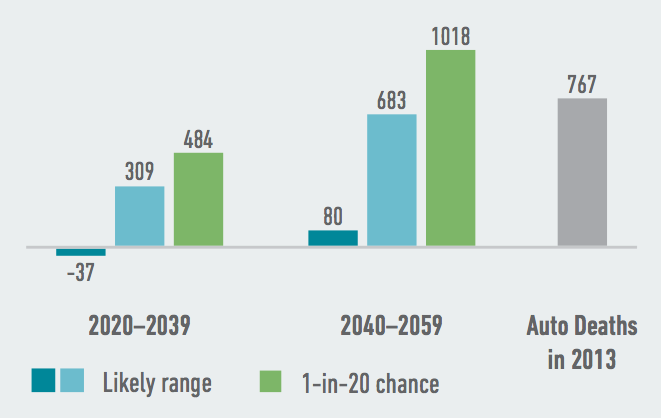

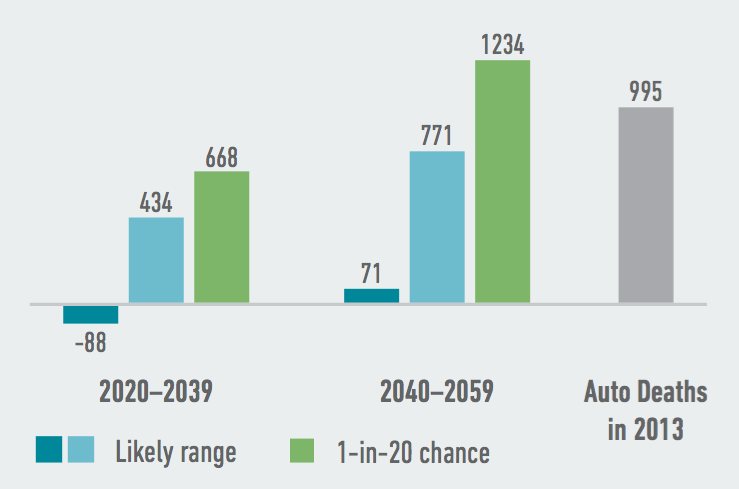

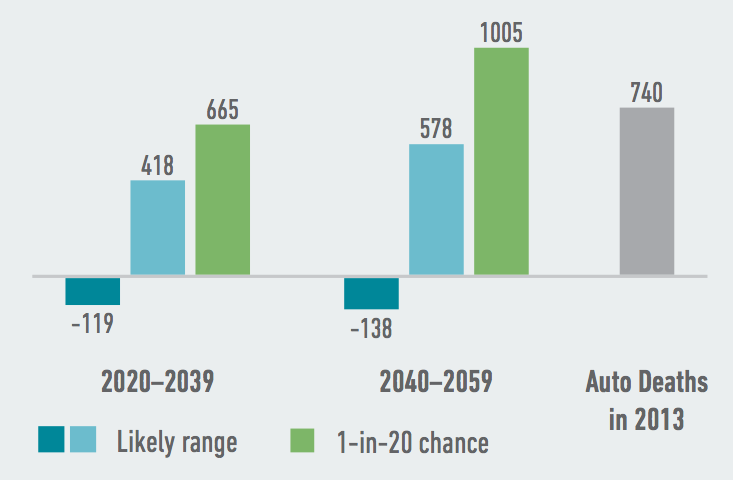

- Rising temperatures will likely increase heat-related mortality and reduce labor productivity across the Southeastern U.S. and Texas.

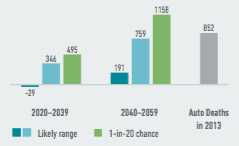

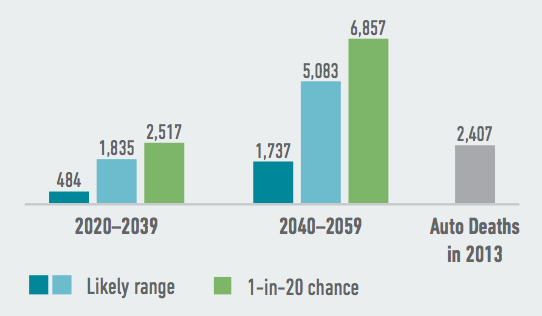

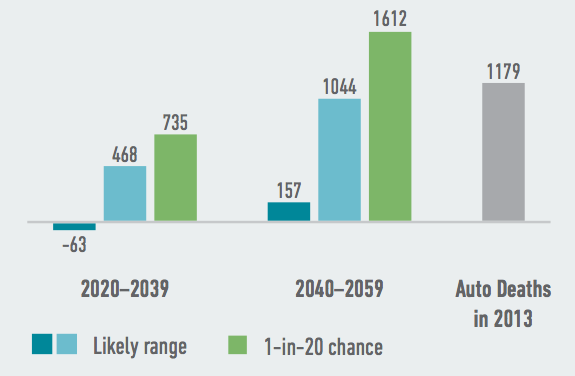

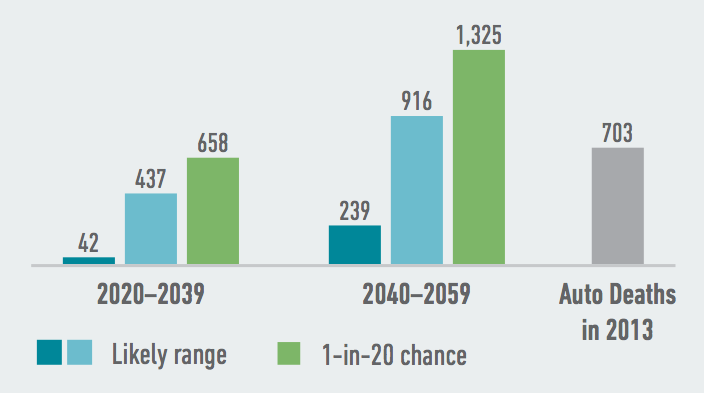

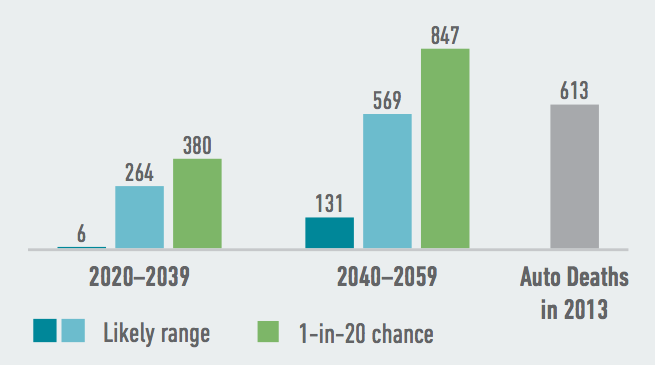

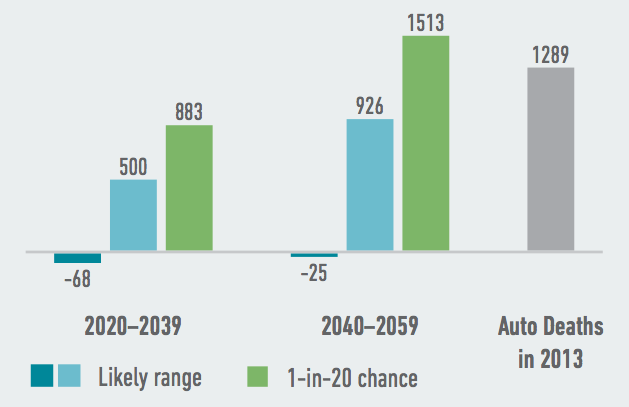

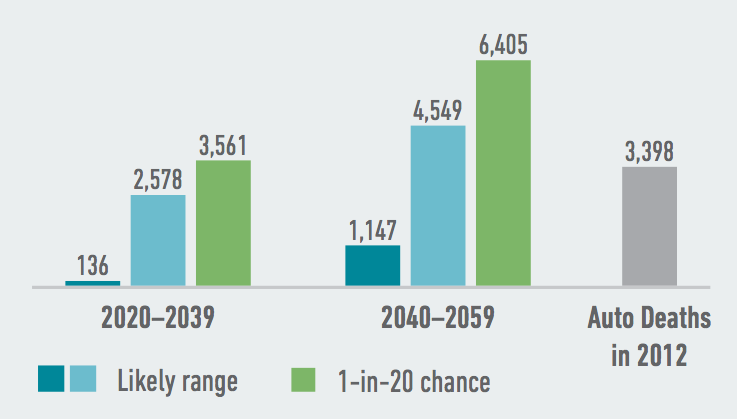

- Over the next five to 25 years, Florida will likely see as many as 1,840 additional deaths per year and Texas, as many as 2,580 additional deaths per year due to extreme heat. By mid-century, these two states combined will likely see as many as 10,000 additional deaths per year. The elderly are most vulnerable to heat-related health risks.

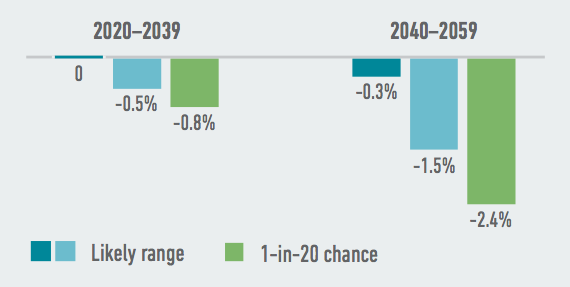

- When the temperature rises past human comfort levels, labor productivity declines, specifically in “high-risk” industries involving outdoor work (which include industries such as manufacturing, agriculture and transportation).

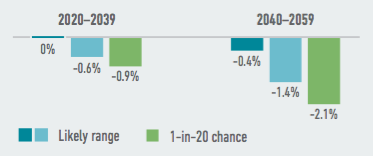

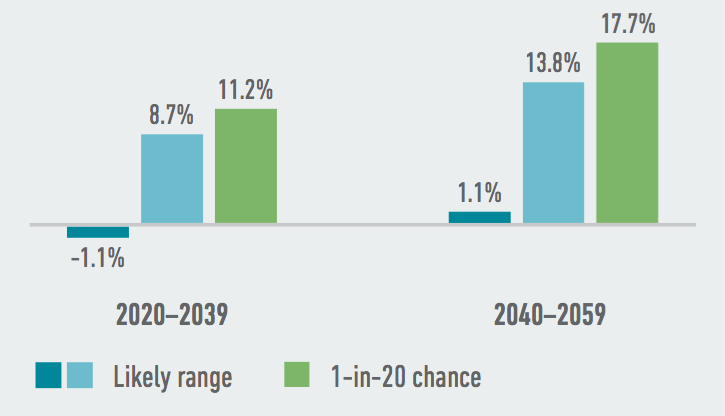

- By mid-century, Southeastern states will likely see labor productivity decline by up to 0.6% on average in these high-risk industries. In Mississippi, there is a 1-in-20 chance that by mid-century the decrease for labor productivity will exceed 2.5% in high-risk sectors.

These diverse impacts from climate change put the Southeastern and Texan economies at risk and could reverse the positive trends seen in the manufacturing sector in recent years. By fully understanding the climate risks these states face if we stay on our current emissions path, Southeastern and Texan businesses and policymakers have the opportunity to become models of climate risk mitigation and resilience.