Drug Channels Institute’s (DCI) latest analysis reveals that more than 33,000 pharmacy locations—more than half of the entire U.S. pharmacy industry—act as contract pharmacies for the hospitals and other healthcare providers that participate in the 340B program. Over the past 12 months, the number of pharmacies in the program has grown by more than 1,000 locations, which was the slowest growth rate since DCI started tracking this figure more than 10 years ago.

Consistent with our previous research, five multi-billion-dollar, for-profit, publicly traded pharmacy chains and PBMs—CVS Health, Walgreens, Cigna (via Express Scripts), UnitedHealth Group (via OptumRx), and Walmart—account for 75% of all 340B contract pharmacy relationships with covered entities. These contract pharmacy operators’ total estimated gross profits from the 340B program were nearly $3 billion in 2023.

Manufacturers’ contract pharmacy policy changes have slowed profits at pharmacies and PBMs, while triggering change in hospitals’ pharmacy strategies. Read on for my latest effort to pierce these little webs of 340B opacity.

FOLKLORE

The 340B program mandates that pharmaceutical manufacturers provide outpatient drugs to certain healthcare providers—known as eligible covered entities—at significant discounts. The Health Resources and Services Administration (HRSA), an agency of the U.S. Department of Health and Human Services, oversees the program through its Office of Pharmacy Affairs (OPA).

Over time, HRSA has introduced subregulatory guidance permitting covered entities to access 340B pricing through an unlimited number of contract (external) pharmacies. The most significant expansion came in 2010, when HRSA issued final guidance permitting covered entities to work with an unlimited number of contract pharmacies. (I remember it all too well.) These actions remain controversial and are the subject of complex, multiparty litigation.

Two other observations on the role of contract pharmacies in the 340B program:

- By using external pharmacies, a 340B covered entity (CE) profits from prescriptions filled by a pharmacy that is not owned or operated by the covered entity. It does this after the prescription has been adjudicated and paid by such third-party payers as Medicare Part D and commercial health plans. (Medicaid prescriptions are excluded by statute. A significant number of Medicaid prescriptions dispensed at contract pharmacies also receive 340B discounts, a.k.a., the “duplicate discount” problem.)

- Contract pharmacies can earn extraordinary profits from the fees paid by a 340B-qualified entity. See my follow-the dollar math in How Hospitals and PBMs Profit—and Patients Lose—From 340B Contract Pharmacies. I discuss the top five players’ profit below.

1989 (AND COUNTING)

In profiling the 340B contract pharmacy market, Drug Channels Institute examined HRSA’s Contract Pharmacy Daily Report, as published on July 1, 2023. We screened out all contracts that had been terminated before that date. Using our proprietary database, we classified all contract pharmacy locations by parent organization. Most chains and many PBM-owned pharmacies are listed with multiple alternate names.

Since HRSA’s 2010 change in guidance, the number of pharmacy locations in the 340B program has skyrocketed.

[Click to Enlarge]

Here are some observations on this never-ending growth:

- In 2010, fewer than 1,300 unique locations acted as 340B contract pharmacies.

- By 2013, we found more than 12,000 340B contract pharmacy locations. This was DCI’s first public analysis of the contract pharmacy market.

- As of mid-2023, DCI counted 33,043 unique locations—a figure far beyond HRSA’s wildest dreams from 2010—acting as 340B contract pharmacies for 340B covered entities. Since our 2022 analysis, the number of 340B contract pharmacy locations has grown by about 1,100 locations (+3%).

- These more than 33,000 pharmacies have 194,016 contractual relationships with 9,585 340B covered entities, i.e., there are more than 194,000 unique contract pharmacy/covered entity relationships. The number of contractual relationships has grown more quickly than has the number of contract pharmacy locations. Since our 2022 analysis, the number of contractual pharmacy relationships has grown by about 25,500 relationships (+15%).

BTW, I’ve been the anti-hero highlighting the out-of-control 340B market for more than 10 years. Check out 2013’s prescient The Coming Battle Over 340B Contract Pharmacies.

FEARLESS (ADAM’S VERSION)

Consistent with our previous analyses, companies with retail pharmacies account for a majority of the 340B program’s total contract pharmacy locations. These companies include Walgreens, CVS Health, Walmart, Rite Aid, Kroger, and Albertsons.

However, the number of locations provides a misleading picture of the 340B contract pharmacy marketplace. That is because an individual contract pharmacy location can have relationships with multiple covered entities. A typical mail and specialty location operates as a 340B contract pharmacy for hundreds of covered entities. By contrast, a typical retail pharmacy location operates as a contract pharmacy for fewer than five covered entities.

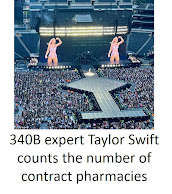

The chart below shows the five largest contract pharmacy participants based on the total number of relationships with 340B covered entities. These companies are also among the largest U.S. pharmacies by prescription revenues. For 2023, these companies accounted for 75.4% of total contract pharmacy/covered entity relationships. That’s an increase from the top five’s share of 73.2% for 2022.

[Click to Enlarge]

These data highlight the complex ways in which the 340B program interacts with the pharmacy and PBM industries:

- Walgreens and CVS Health remain the two most active 340B contract pharmacy participants. Each company has more than 8,200 locations participating as 340B contract pharmacies. They each are partnered with more than 3,000 340B covered entities.

- Two other large PBMs—the Express Scripts business of Cigna and the OptumRx business of UnitedHealth Group—are among the most active participants when measured by the number of 340B contract pharmacy agreements with covered entities. Each company has partnered with about 1,500 340B covered entities.

- The three largest PBMs—CVS Health, Express Scripts, and OptumRx—collectively have about 230 mail, specialty, and infusion pharmacy locations acting as 340B contract pharmacies. Combined, these locations have nearly 43,000 relationships with covered entities. Consequently, the big three PBMs’ non-retail pharmacies account for less than 1% of 340B contract pharmacies—but 22% of 340B contract pharmacy relationships.

Note that OptumRx also operates more than 700 community pharmacies. Most of these locations are operated by Genoa Healthcare, which OptumRx acquired in 2018.

Twenty-three manufacturers have altered policies related to covered entities’ contract pharmacies in the 340B Drug Pricing Program. Specific policies vary by company, but generally include some or all of the following policies:

- Requiring a covered entity to use an on-site pharmacy and/or designate a single, external contract pharmacy

- Limiting the geographic scope of contract pharmacies relative to the covered entity’s physical location

- Requesting or requiring that the covered entity share deidentified claims data in order for those claims to be eligible for 340B discounted pricing. Many manufacturers have asked covered entities to use the 340B ESP platform to share claims data.

- Some manufacturers have applied these conditions only to hospitals and have excluded federal grantees. Others have applied these conditions to all type of 340B covered entities. These limits have curtailed the number and volume of 340B prescriptions that were handled by contract pharmacies.

These restrictions have had multiple market impacts:

- 340B-eligible purchases at contract pharmacies have slowed. Per IQVIA, growth in 340B-purchases at retail and mail pharmacies has slowed sharply, from year-over-year growth of 36% in 2020 to just 5% growth in 2022. (See page 5 of The 340B Drug Discount Program Exceeds $100B in 2022.) I presume purchases of 340B-priced products declined for the products of manufacturers with 340B contract pharmacy restrictions.

- Profits for 340B contract pharmacies have declined (a little). Contract pharmacies can earn 25% to 35% of total 340B discounts.

According to Nephron Research, the five largest contract pharmacy operators’ total estimated gross profits from the 340B program peaked in 2021, at $3.2 billion. These companies’ estimated profits from the program will decline to an estimated $2.9 billion for 2023, due to the manufacturer policy changes. However, these are champagne problems when we consider that estimated profits were only $1.1 billion in 2017. (Please contact info@nephronresearch.com for more details on Nephron's 340B gross margin model.)

As I explain in Section 11.5.5 of our 2023 pharmacy/PBM report, these companies seem to share their 340B profits with plan sponsors by accepting lower reimbursement rates for preferred participation in narrow networks.

- The largest public companies have had to acknowledge the previously-hidden profitability of the 340B program. Manufacturers’ policy changes have forced some long-overdue transparency about 340B contract pharmacy profits.

In May, CVS Health disclosed that 340B contract pharmacy changes would lower its PBM segment profits by $150 to $200 million.

Last year, Walgreens disclosed that manufacturers’ disruptions to the 340B contract pharmacy market will reduce its profits by about $250 million in the company’s 2022 and 2023 fiscal years. But on its most recent earnings call, Walgreens planned to shake it off, stating it is “very comfortable with our prior guidance and do expect 340B to actually be a slight up in production year over year in fiscal '23.”

- Hospitals are investing more in their in-house specialty pharmacies. In recent years, health systems and hospitals have become direct participants in the specialty pharmacy market by operating internal pharmacies. (See Exhibits 51 and 55 of our 2023 pharmacy/PBM report. As I have been predicting for some time, the changes in manufacturers’ 340B contract pharmacy policies have accelerated hospitals’ investments in in-house specialty pharmacy operations.

- PBMs have gained 340B market share. When forced to choose a single contract pharmacy partner, we believe that hospitals and health systems have been gravitating to the large PBM-owned specialty pharmacies. These pharmacies have superior access to drugs in limited dispensing networks. (See Exclusive: Profiling Manufacturers’ Limited and Exclusive Pharmacy Networks for Specialty Drugs.)

Consequently, PBMs have gained a greater share of overall 340B contract pharmacy business, even as the overall contract pharmacy business slows. Unfortunately, there are no public data to confirm this observation.

Despite the size and growth of the 340B contract pharmacy market, evidence from three separate government studies shows that most 340B hospitals do *NOT* provide discounts to low-income, uninsured patients at their facilities' contract pharmacies. (See the links provided in my May 2023 news roundup.) This shameful reality reflects the fact that the 340B Drug Pricing Program lacks a regulatory infrastructure, has few administrative controls, and contains too many blank spaces in the legislation.

The ongoing profiteering by 340B contract pharmacies, combined with the perilous legal situation, may finally encourage legislation to fix this out-of-control program and reign in contract pharmacies. Hospitals' 340B program abuses have also led to bad blood with federal grantees, some of which have partnered with manufacturers to form The Alliance to Save America’s 340B Program.

It’s been said that there are no rules in breakable heaven. But I think it could be a cruel summer for covered entities.

ACKNOWLEDGEMENTS

No comments:

Post a Comment